Understand the Facts about Long-Term Care; It Affects Everyone!

The statistics regarding the risk of needing and using long-term care services are alarming. As the population ages and life expectancy increases, the number of individuals at risk will also rise. First, the elderly population is growing. By 2030, it is projected that the number of individuals aged 65 and older will exceed 71 million, nearly double today's figure. Second, according to the U.S. Department of Health and Human Services, approximately 70 percent of individuals over 65 will require at least some form of long-term care services during their lifetimes. Third, more than 40 percent will need care in a nursing home for some period.

Who Is at Risk?

It is understandable that many people associate the need for long-term care primarily with the elderly. However, an article prepared for the Georgetown University Long-Term Care Financing Project reveals that nearly 40 percent of individuals requiring long-term care are age 40 or younger. In younger age groups, congenital defects and accidents are the main causes that lead to the necessity for long-term care. During middle age (45 to 55), congenital diseases increase this risk. After 70, people face the same congenital diseases as well as various health conditions and frailty.

Other facts and statistics about long-term care indicate its increasing prevalence:

Over 6 million elderly Americans require assistance from family or friends to remain in their homes. At least two-thirds of all home-care help is provided at no cost by family members and friends.

Of people turning 65, 69 percent will need some long-term care before they die.

More than half of the U.S. population will require some form of long-term care, including nursing home care, home health care, assisted living, or care at a rehabilitative facility.

Of men reaching 65, 58 percent will require some long-term care.

Women face a higher risk than men—after they turn 65, 79 percent of women will need some form of long-term care at some point before death. Among those reaching 65, 52 percent will require long-term care for at least one year before their passing, and 20 percent will need more than five years of care.

The average stay in a nursing home is about two and a half years.

Starting in 2021, the number of people in nursing homes is expected to rise significantly, as this marks the year when the oldest baby boomers will turn 75.

Studies have predicted that the nursing home population will expand to between three and four million residents as the population ages.

When to Purchase Long-Term Care Insurance

Since premiums tend to rise significantly with issue age, deciding when to buy LTCI is a crucial consideration. When we are young and healthy, most of us do not think about our health in the years or decades ahead. It seems even harder to envision a serious illness or injury that could require long-term care. However, when we are fit and well, it is the right time to consider purchasing long-term care insurance. The typical LTCI buyer is between 55 and 60, and the average issue age has been decreasing in recent years. Many companies target customers as young as 40. Because premium costs rise based on an individual's age at issue, the younger the applicant is when purchasing the policy, the lower the premium will be throughout the life of the plan. Premiums typically remain consistent each year, except when insurers raise rates for an entire class of insureds. Therefore, experts suggest that individuals begin considering LTC much earlier than they actually need it.

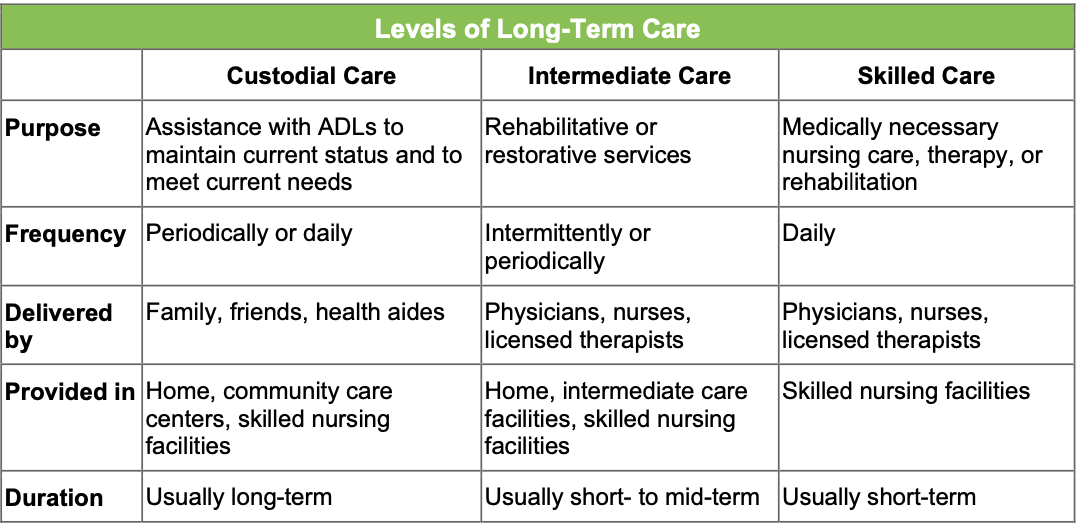

Types and Levels of Care

Long-term care encompasses various services designed to assist individuals with chronic conditions in managing limitations they face in functioning independently. Those requiring long-term care present diverse physical and mental challenges that necessitate different types and levels of support. Consequently, the long-term care sector has introduced new terminology to describe the settings and methods of care delivery.

First, long-term care can occur in several environments, including:

Individual’s home

Community Locations Adult Day Care (ADC)

Assisted Living Facility (ALF)

Skilled Nursing Facility (SNF)

Genworth Financial, Inc., Cost of Care Survey 2023

Receiving care and services at home or in a community setting allows individuals to remain in their homes rather than being moved to a nursing facility or another full-time residence. A key aspect of managing long-term care is empowering those who wish to stay in their homes, enabling them to do so while maintaining their independence for as long as possible. The median cost estimates are from Genworth Financial, Inc., Cost of Care Survey 2023.

Home Health Aide and Homemaker services provide assistance with “hands-off” tasks such as cooking, cleaning, and running errands, with a median cost of $68,600 per year.

Home Health Aid offers “hands-on” personal assistance with activities like bathing, dressing, and eating, with a median cost of $75,500 per year.

Median Cost of Adult Day Health Care is $85 per day nationally and $130 per day in Washington.

Median Cost of Assisted Living Facilities is $57,300 per year nationally and $76,400 per year in Washington.

Median Cost of Nursing Home Care is $100,700 per year for a semiprivate room and $115,000 per year for a private room nationally, with costs in Washington at $120,000 per year for a semiprivate room and $133,200 per year for a private room.

Who Pays for Long-Term Care

The sources of paying for long-term care break into four categories:

Individual/personal resources

Medicare

Medicaid

Long-term Care Insurance

Individual/Personal Resources:

About 20 percent of long-term care costs are covered by recipients using their personal savings, income, and assets. However, many quickly deplete their financial resources since this type of care is quite costly.

Medicare:

For those who are eligible, Medicare sometimes pays for short-term care in a skilled nursing facility but does not cover extended care. Medicare coverage for skilled nursing facility (SNF) care does not extend beyond 100 days, effectively excluding Medicare, Medicare supplements, and Medicare Advantage (Part C) as sources of long-term care funding, except in very limited cases.

Medicaid:

About 45 percent of long-term care costs are covered by Medicaid. However, Medicaid is only available to individuals with low incomes and limited assets; to qualify, many must go through the process of “spending down” their personal resources to nearly poverty levels. To accept Medicaid patients, a facility or service provider must be approved by Medicaid. Likewise, Medicaid patients typically do not have the option to choose where they receive their care; they must go to a Medicaid-approved facility or provider.

Long-Term Care Insurance:

Long-term care insurance is designed specifically to cover the expenses associated with custodial, intermediate, and skilled nursing care. Policies are available to fund care provided at home, in the community, and in formal facilities. Importantly, while the risk and costs of long-term care are substantial, the one source explicitly meant to address this need—long-term care insurance—represents a very small portion of LTC payments.

Breaking Down the Cost

In 2021, Medicaid accounted for the largest share of long-term expenditures, covering 44.3 percent of total costs. Other public programs contributed 27 percent, while consumers paid nearly 14 percent of the nation’s long-term care expenses out of pocket. Among the smallest contributions was from private long-term care insurance, which represented only 8 percent. Overall, long-term care spending from all these sources reached $467 billion in 2021. The cost of care provided by unpaid, informal caregivers—such as family and friends—is not included in this total. The economic value of this “donated” care is estimated to be worth billions of dollars.

Long-term care insurance is not auto or home insurance!

When considering the purchase policy, such as a homeowner’s or auto policy, the buyer likely assumes that the insured risk will never happen. To grasp this, consider how rarely we hear of a house fire compared to the many homes we see daily or how infrequently we experience an auto accident—an insurance policy given the thousands of hours we spend in our vehicles. Nevertheless, homeowner and auto insurance policies remain pretty standard.

Nonetheless, the risks associated with long-term care differ considerably. Insurers and policyholders rely on distinctly different statistics. More than half of the U.S. population will need some long-term care during their lifetimes, whether it involves nursing home care, home health care, assisted living, or care in rehabilitation facilities. The likelihood of requiring long-term health care is significant; it presents a 50/50 chance.

Individual Options, covering the cost of LTC

Individual Long-Term Care Insurance:

An individual Long-Term Care Insurance (LTCI) policy is a contract between the insurer and the individual policyholder. Underwriting is conducted on an individual basis, with policies typically issued on a preferred, standard, or substandard basis depending on the insured’s physical and mental health status. For some insurers, the insured’s risk classification influences the premium charged; a nonstandard or substandard rating, for example, may necessitate a higher premium (or limited coverage). For other insurers, an applicant’s health condition solely determines whether a policy will be issued. As noted earlier, most individual LTCI policies are guaranteed renewable and cannot be canceled by the insurance company unless the premium is not paid on time. However, each company retains the right to increase premiums charged to an entire group of insured individuals with appropriate notification and approval from the state in which it operates.

Linked Benefit/Hybrid Life Insurance and Annuity Policies:

One of the latest innovations in the LTCI industry is a linked benefit or hybrid policy that merges the features of LTCI with life insurance or an annuity contract. Compared to stand-alone LTCI policies, these hybrid policies offer some cash value and provide a death benefit. If long-term care is not needed, the cash value of the base policy or contract can be accessed or passed on to a beneficiary upon the death of the insured or contract holder owner.

Long-Term Care Insurance Partnership Plans:

As the demand for long-term care continues to rise, already a significant national expense, federal and state policymakers are seeking changes in the financing of that care. If there is no shift in how the high costs of care are covered, the two groups that can least afford it—consumers and state Medicaid programs—will keep bearing the brunt. This poses a significant issue. With long-term care financing being a major factor, state budgets nationwide are already burdened by Medicaid’s demands. They are ill-equipped to handle any additional strain. Consumers, who are already grappling with their current expenses, have little ability to take on more of the long-term care financing responsibilities. Transferring the burden of long-term care financing from states to an industry focused on managing financial risk makes so much fiscal sense that it underpins the “Partnership for Long-Term Care” initiative, an innovative insurance program launched in 1988 with support from the Robert Wood Johnson Foundation. The program encourages consumers to purchase affordable long-term care insurance policies, alleviating the pressure on state Medicaid programs.

Conclusion

Long-term care insurance can help protect individuals, their families, and their assets against the potentially catastrophic cost of extended care by providing the funds to meet expenses when the time comes.

The cost of long-term care services has risen across all provider types, with certain providers experiencing more significant increases. The most notable cost hikes were seen in home health aide and homemaker services. Inflation and a shortage of skilled care workers are the primary factors driving up the costs of care services. Understanding long-term care options and the associated costs is a critical first step in preparing for your aging journey.

Hybrid permanent life insurance and long-term care (LTC) is a policy that combines life insurance with long-term care coverage, offering benefits for both. Contact me to learn how this combination can provide essential living benefits through guaranteed permanent life insurance.