Managing Long-Term Care Expenses in Washington

Intro: State and federal authorities collaborate to shift long-term care financial responsibilities from states to a financially savvy industry. This strategy forms the basis of the Partnership for Long-Term Care, which is recognized for its strong fiscal framework. Moreover, these partnership initiatives expand Medicaid's coverage to include the long-term care insurance (LTCI) sector, positioning it as an additional payer alongside Medicaid beneficiaries, i.e., individuals who receive health insurance benefits through Medicaid.

Washington State Medicaid is a government health insurance program that serves individuals with limited income and resources. Established by Title XIX of the Social Security Act, Medicaid was enacted in 1965 concurrently with Medicare. Every state, District of Columbia, and U.S. territories operate Medicaid programs to provide health coverage for low-income individuals. While the federal government sets specific guidelines for all states to adhere to, each state administers its Medicaid program uniquely, leading to differences in Medicaid coverage nationwide.

States have consistently taken a straightforward approach to Medicaid cost recovery: shifting part of the financial responsibility to the Medicaid beneficiary through Medicaid's asset and income spend-down rules. These rules require beneficiaries to deplete nearly all personal income and assets (or assign them to the state) in exchange for Medicaid coverage of long-term care needs. Only a nominal amount, approximately $2,000 or $3,000 in assets, can be retained. Furthermore, when a Medicaid long-term care recipient passes away, a state may recover the costs incurred in providing that care from the recipient's estate. This may be of little concern to those with limited or no personal assets. Still, these spend-down and recovery rules can be an overwhelming burden for individuals and families with even modest means.

Since the demand for long-term care, which is already a significant national expense, is expected to rise dramatically, federal and state policymakers have been pursuing changes in how that care is financed. If the high cost of care is not addressed, the two parties least able to afford it—consumers and state authorities—will bear the burden. Medicaid programs will continue to bear the brunt of this situation, presenting a significant challenge. Long-term care financing is a major factor, and state budgets across the country are already strained under Medicaid’s weight and cannot bear any further increase in that burden.

Consumers who already find it challenging to cover their current share cannot take on additional responsibilities for long-term care financing. The idea of shifting the financial burden of long-term care from the states to an industry experienced in managing financial risk is so fiscally sensible that it forms the basis of the “Partnership for Long-Term Care" initiative, a unique insurance program launched in 1988 under the sponsorship of the Robert Wood Johnson Foundation. The program aims to encourage consumers to purchase affordable long-term care insurance policies and reduce the strain on state Medicaid programs.

LTC Partnership Program Purpose: Shift Financial Responsibility to Insurers

Partnership programs redefine Medicaid’s “other payer" to include the long-term care insurance (LTCI) industry. Individuals with a partnership-qualified long-term care insurance policy may still be liable for some long-term care costs. Still, they apply for Medicaid coverage only after policy benefits are exhausted. Even in that case, a significant portion of the individual’s assets will be protected, thanks to the Medicaid spend-down exemption feature common to all state partnership plans

Washington State Long-Term Care Partnership Programs

The Washington State Long-Term Care Partnership (LTCP) offers consumers an additional option to assist with long-term care expenses, including nursing home care and home-based care. It helps you avoid spending down or transferring assets to qualify for Medicaid when assistance is needed for at least two activities of daily living (ADLs).

Long-Term Care Insurance (LTCI) Partnership Plans

The Deficit Reduction Act (DRA), signed into law on February 8, 2006, included Section 6021. This provision authorized states to offer special Medicaid asset disregards for individuals purchasing and utilizing qualified private long-term care insurance policies, commonly referred to as 'Partnership' policies. The Long-Term Care Partnership Program is a joint federal-state policy initiative designed to promote the purchase of private long-term care insurance and expand access to policies that cover long-term care services.

Purchasing a Partnership-qualified (PQ) long-term care insurance policy provides an extra benefit. This benefit is known as “dollar-for-dollar” asset disregard or “spend down” protection. Individuals who buy a PQ policy 'earn' one dollar of Medicaid asset disregard for every dollar of insurance coverage paid on their behalf.

Here's an example: Jane purchases a PQ policy and one day requires care. Her policy pays out $150,000 in insurance claim benefits. Stephanie receives a Medicaid asset disregard that allows her to retain an additional $150,000 above the asset level she would otherwise need to meet to qualify for Medicaid coverage. The Partnership Program also safeguards those assets after death from Medicaid estate recovery.

Linked Benefit/Hybrid Life Insurance and Annuity Policies

One of the latest innovations in the LTCI industry is a linked benefit or hybrid policy that merges the features of LTCI with life insurance or an annuity contract. Unlike stand-alone LTCI policies, these hybrid options have some cash value and offer a death benefit. If long-term care is unnecessary, the cash value of the base policy or contract can be accessed or bequeathed to a beneficiary upon the insured's or contract owner’s death.

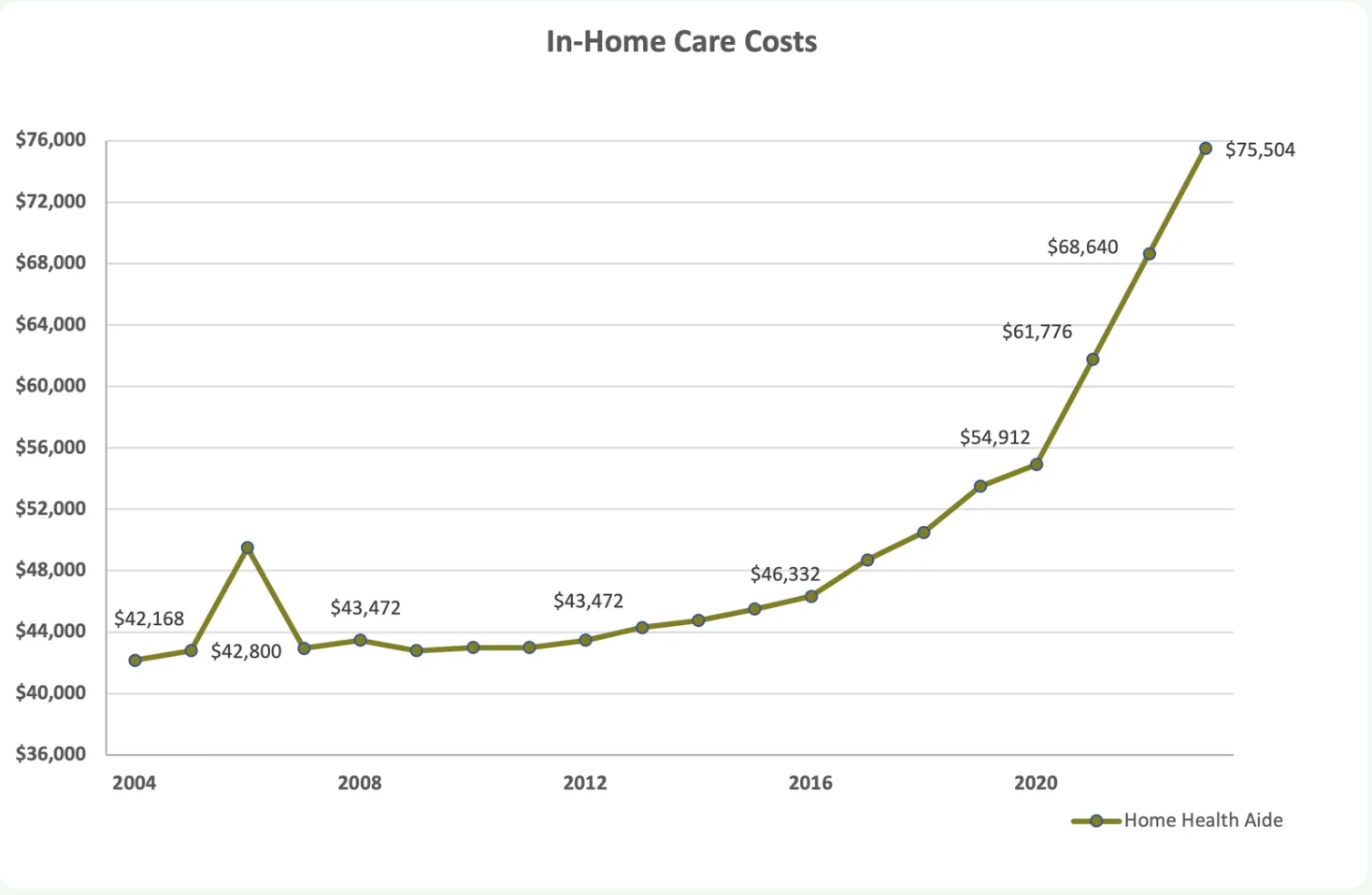

Average Long-Term Care Costs, Source: Genworth 2023 Cost of Care

Average Long-Term Care Costs, Source: Genworth 2023 Cost of Care

Average Long-Term Care Costs, Source: Genworth 2023 Cost of Care

Washingtons Cares Fund

The WA Cares Fund is the result of years of research aimed at making care accessible for all workers in Washington. As a public long-term care insurance program, WA Cares guarantees coverage for all workers, regardless of pre-existing conditions. Washington is the first state in the nation to offer an affordable option for the broad middle class to access long-term care without draining their life savings. The WA Cares Fund is administered by the Washington State Department of Social and Health Services in partnership with the Washington State Health Care Authority and the Employment Security Department, ensuring that working Washingtonians can obtain a modest amount of long-term care when necessary.

Starting in July 2023, Washington workers will contribute up to 0.58 percent of their wages to the program. Only employees are required to contribute; employers do not participate. Contributions will continue as long as workers are employed in Washington state.

Starting in July 2026, eligible individuals can access up to $36,500 in lifetime benefits from the program. To qualify for these benefits, a person must be at least 18 years old, currently reside in Washington, have contributed to the program for a minimum of ten years, and require assistance with at least three activities of daily living. Participation is required; however, there are exceptions. For example, individuals who purchased a qualified private long-term care policy before November 2021 may apply for a permanent exemption from the program.

Genworth Washington State 2023

Website Links