The Rise and Fall of Pension Plans Part 2

The Retirement Crisis is a global emergency. To understand why our retirement system is failing in the United States, it is best to understand what other countries are doing better than we are. The Mercer CFA Institute Global Pension Index 2023 is an excellent place to start. It compares 47 countries’ retirement income systems for adequacy, sustainability, and integrity. Shockingly, the United States ranks 22nd out of 47 countries in retirement.

Providing financial security in retirement is critical for individuals and societies, as most countries are now grappling with the social, economic, and financial effects of aging populations. The World Economic Forum noted: “For the first time in human history, people aged 65 and over outnumber children aged five or younger.”

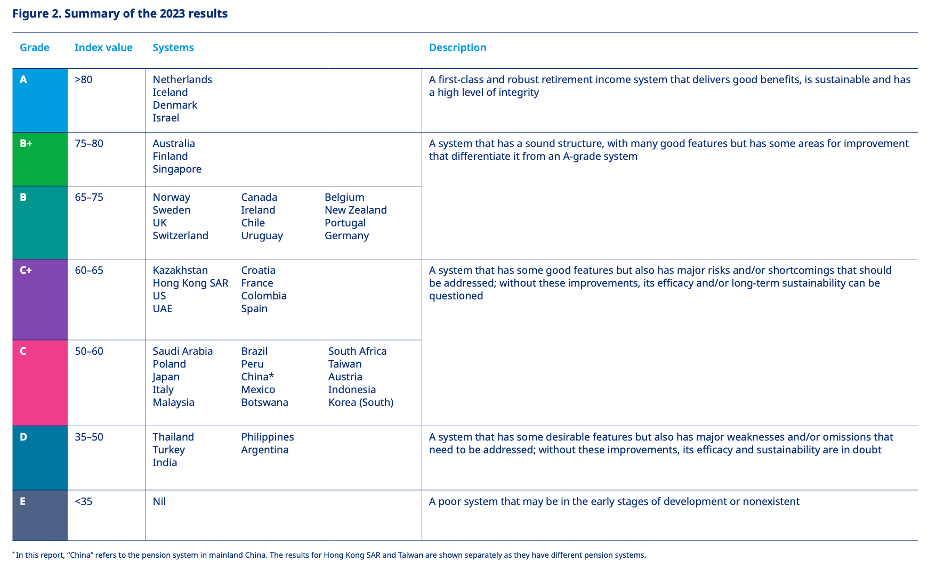

Summary of the results Mercer CFA Institute Global Pension Index 2023

Summary of the results Mercer CFA Institute Global Pension Index 2023

* In this report, “China” refers to the pension system in mainland China. The results for Hong Kong SAR and Taiwan are shown separately as they have different pension systems. - Mercer CFA Institute Global Pension Index 2023

Let's examine some of the top Global Pension Index performers and look for similarities and differences. The three examples we will use are #1, Netherlands, #3, Demark, and # 5, Australia versus #22, United States.

#1 Netherlands Pensions System Population 18,249,057 (2024)

The Dutch pension system combines a pay-as-you-go system, where workers pay for retirees' benefits, and an individual investment system.

1. State Pension System

2. Private Pension System regulated by pension law,

3. Individual Private Pension.

#3 Denmark’s Pension System Population 5,981,460 (2024)

Denmark's Gross Savings Rate was 28.6% in March 2024

The Danish pension system is designed so that you can receive a pension from multiple sources.

1. Statutory Pensions are (state pensions and disability pensions)

2. Labor Market Pensions (part of your employment contract)

3. Individual Pensions (set up yourself via a pension company or bank)

#5 Australia Pension System Population 26,758,006 (2024)

Australia has a three-tier pension system.

1. A public tax-financed Age Pension, which provides essential benefits.

2. Superannuation funds offer a funded individual pension account (money set aside while you're working that you can access later when you retire).

3. Individuals contributing to their superannuation funds or Retirement Savings Accounts (RSAs).

# 22 United States Population 345,744,905 (2024)

1. Social Security is funded primarily through payroll taxes. It provides replacement income for qualified retirees and their families.

2. Defined Benefit Plan (Pensions): promises a specified monthly benefit at retirement. The benefits in most traditional defined benefit plans are protected, within certain limitations, by federal insurance provided through the Pension Benefit Guaranty Corporation (PBGC).

3. Defined Contribution Plan: It does not promise a specific retirement benefit. In these plans, the employee or the employer (or both) contribute to the employee's account under the plan. These contributions generally are invested on the employee's behalf. The employee will ultimately receive the balance in their account based on contributions plus or minus investment gains or losses. The account's value will fluctuate due to the changes in the value of the investments. Examples of defined contribution plans include 401k, 403b, employee stock ownership, and profit-sharing plans.

Similarities are evident when comparing the retirement plans of the top countries (Netherlands, #3, Demark, and # 5, Australia) with those of the United States. All countries have at least three categories: government, employer, and Individual. At first glance, in top-rated countries, pensions drive retirement. In contrast, in the United States, in March 2023, 15% of private industry workers had access to a defined benefit plan (pension), and the personal savings rate was 3.9% of their income. However, this doesn't distinguish between general and other savings types, like retirement. In contrast, the top Global Pension Index performers, on average, save 20% of their income.

In the United States, Social Security remains the most common source of retirement income, and 80 percent of retirees have one or more private income sources. This included 56 percent of retirees with income from a pension, 48 percent with interest, dividends, or rental income, and 33 percent with labor income (such as wages, salaries, or self-employment income)

Some shocking statistics

Today, on average, Social Security replaces 40% of an individual’s annual salary in retirement. Nearly 58 million adults age 65 and older live in the U.S. in 2022, accounting for 17.3% of the nation's population. An additional 30.2 million will retire between 2025 and 2030. It's estimated that two-thirds of those retirees will only have Social Security as their prime source of income.

Annuities, a key component of pensions, gained prominence in the early 20th century to provide a steady income for life. However, with the recent shift from defined benefit plans to defined contribution plans, the traditional pension model has been gradually phasing out. The rise of 401k plans and other retirement savings vehicles has altered the retirement landscape, offering individuals more control over their investments and exposing them to market risks. As a result, the guaranteed income for life that pensions and annuities once provided is becoming increasingly rare.

The Best Retirement Countries use Annuity-Based Guaranteed Income. Norway citizens, on average, save 20%, and the US saves 3% at a national average. The average rate of return for a typical 401k over several decades is 5% and 8% before retirement taxation.

Hitting the $1 million milestone in your 401k isn’t as great as you think. For generations, $1 million stood as the signifier of a secure retirement and a lofty target. But between taxes and inflation, the million-dollar question is just how much value that number holds now. Today, $1 million has a buying power of roughly $600,000 in 2004.

According to Vanguard's How America Saves report, the median 401(k) balance among Americans 65 and over with defined contribution plans is just $70,620. Low 401(k) balances and limited Social Security left as many as 8 million seniors in poverty in 2022.

Considering all this and adding my personal experience, these are the areas you need to adjust as individuals: saving more, not relying solely on 401k, and factoring in inflation/taxes early on in retirement planning.

1. Critical: Saving More – 10% to 15%+ is the new standard. Adjust your living style to accommodate.

2. Diversity: Retirement Income Streams – 401k/IRA’s, Personal Pension, Social Security.

3. Mitigate: Inflation/Taxes – Make it a significant factor in your retirement planning.

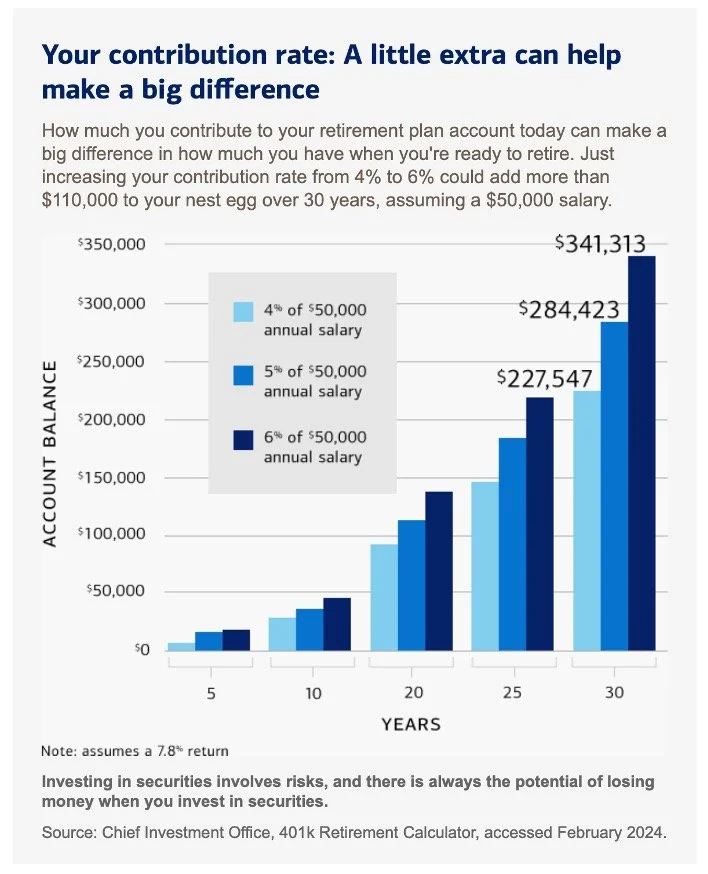

Contribution - a little extra makes a big difference